Thank you for your proposal.

Holding stablecoins in the treasury is certainly one approach to maintaining stability.

From my understanding, this proposal goes a step further by suggesting a dual-token system involving a governance token and a stablecoin. Several blockchain projects have already implemented similar systems.

Algorithmic Stablecoins

- Terra: UST (Collapsed)

- Near: USN

- Tron: USDD (Transitioned to an overcollateralized model)

Overcollateralized Stablecoins

- Acala: aSEED (Currently depegged due to a hack)

- Berachain: HONEY (Currently backed by USDC and BYUSD)

Algorithmic stablecoins can be extremely powerful if they succeed, but very few have worked out, making them excessively high-risk. If Astar were to shift in that direction, I would likely step away from the project.

On the other hand, issuing an overcollateralized stablecoin and holding it in the treasury is essentially equivalent to holding the collateral itself. If the issued stablecoin is used for operations, it may appear as if governance tokens are not being sold. However, in a DeFi environment, the sell path often ends up being stablecoin → governance token → cash, leading to an indirect governance token sell-off. For this to work, the native stablecoin would need to be widely traded, which is a significant hurdle.

If the goal is to secure additional funding via stablecoins, a more practical approach would be similar to how governments issue bonds or corporations issue corporate bonds. However, without legal enforceability, this is also an unrealistic option.

If an overcollateralized stablecoin must be used, a third-party stablecoin like SONE, which allows collateralization with assets other than ASTR, would provide more stability. Additionally, if the chain itself issues a DeFi product, competition within the ecosystem could be disrupted, making it preferable to rely on third-party solutions. However, the capital efficiency in this model is quite poor.

If the goal is simply to hold stablecoins in the treasury, using a highly liquid and stable option like USDC would be more appropriate. While concerns about centralization exist, centralization often correlates with reliability (depending on the issuer). Since USD-backed stablecoins derive their value from national currencies, this trade-off may be acceptable. The main issue is that converting ASTR into stablecoins periodically equates to continuous sell pressure.

Summary of My Thoughts

If Astar wants to hold stablecoins in the treasury, there are two main options:

- Regularly swap ASTR for stablecoins (but this leads to continuous selling pressure on ASTR).

- Use ASTR as collateral to mint third-party stablecoins (but this favors specific dApps and increases third-party risks).

I don’t see the necessity for a dual-token system, as it would likely introduce more negative consequences than benefits.

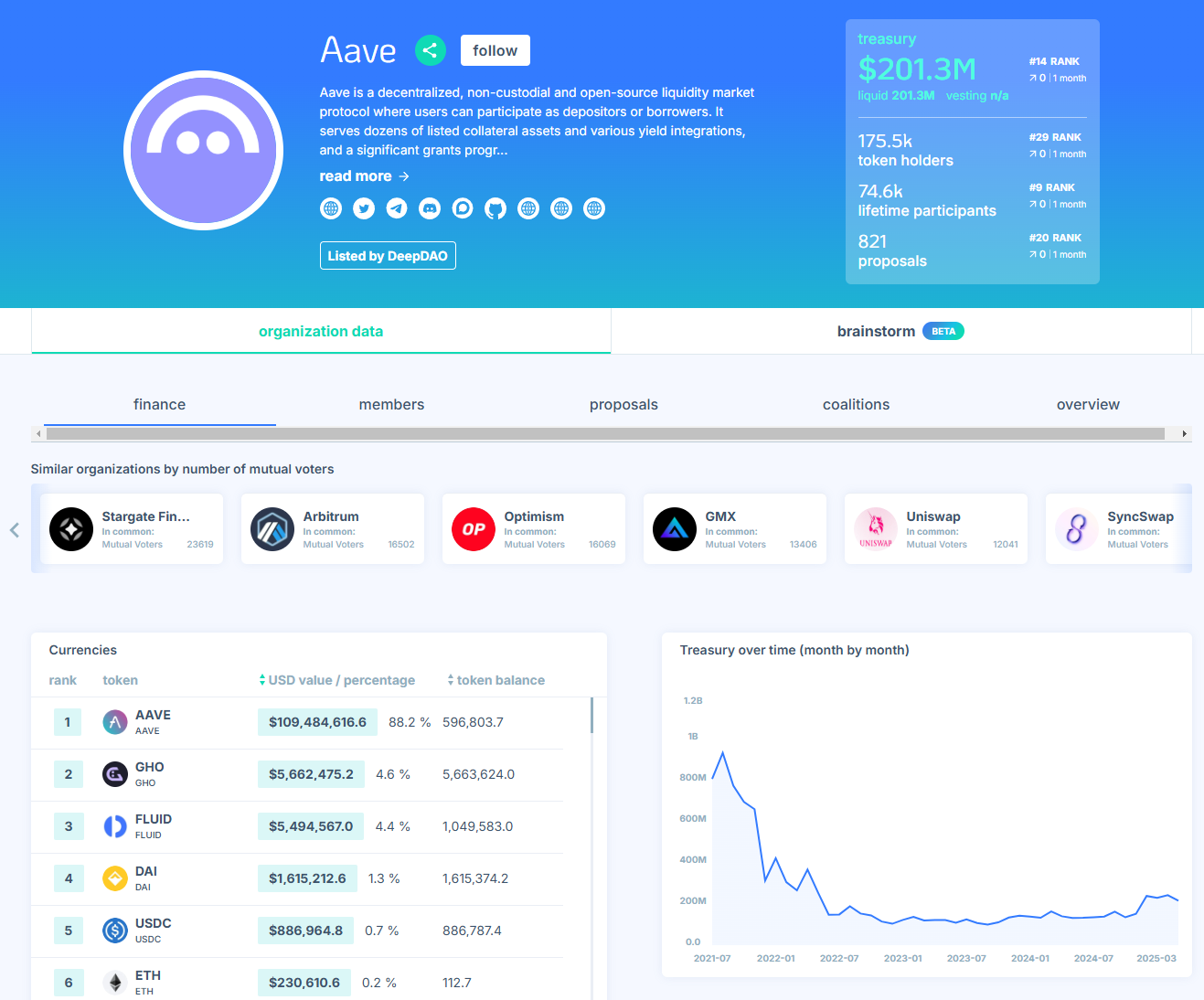

For reference, let’s take a look at how other projects manage their treasuries. Using DeepDAO, we can analyze existing structures.

As you can see, in most projects, over 90% of their treasuries consist of governance tokens—even in DeFi projects with fee revenues. This highlights the difficulty of incorporating stablecoins into a treasury in a sustainable way. Notably, Lido’s treasury is composed of nearly 38% ETH, which suggests that their business model is highly successful.